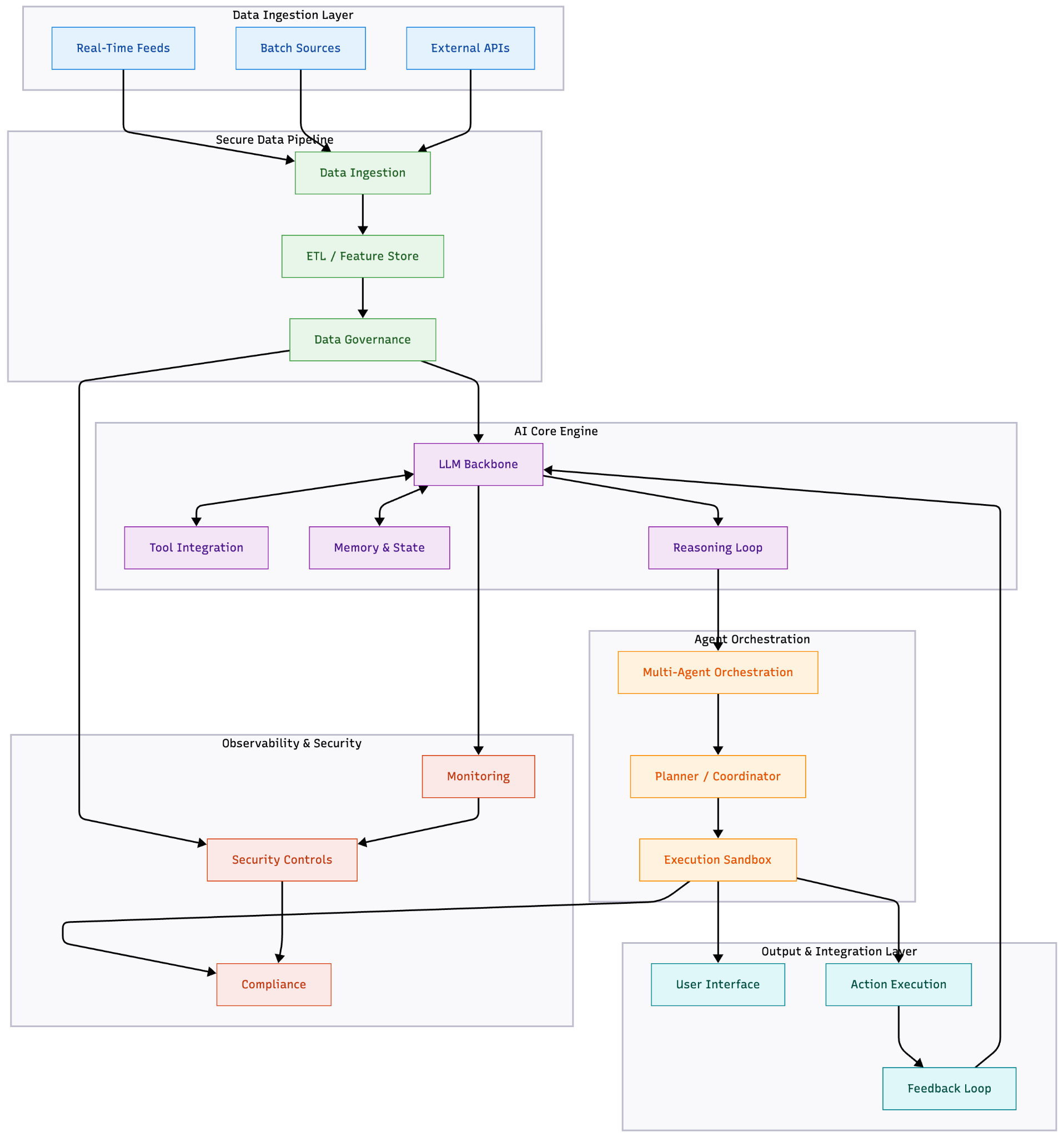

Key use cases of agentic AI in finance

AI agents are rapidly reshaping the finance and banking sector by enhancing autonomy, intelligence, and adaptability. Instead of relying only on rigid rule-based systems, these agents can understand real-time data, make sense of complex financial situations, interact with tools and APIs, and continuously learn from feedback.

Here are some of the key areas where AI agents are already making a meaningful impact.

1. Fraud detection & prevention

Modern financial systems handle massive streams of transactions every second. AI agents help make sense of this chaos by scanning activity in real time, spotting anomalies, and taking action before fraud escalates.

How agentic systems improve fraud detection

AI agents analyze transactions, user behavior, device details, and merchant history. Instead of relying on fixed rules, they generate dynamic risk scores using LLM-based reasoning and anomaly detection models.

When something looks suspicious, the agent can instantly block a transaction, trigger an extra KYC step, or hand the case to a human analyst. With a built-in memory component, these agents also learn new fraud patterns over time.

For example, if a user suddenly initiates rapid micro-transactions, the agent may review prior behavior, query internal risk APIs, and decide whether to flag or block the activity, while automatically documenting the rationale.

Real-world examples:

- Major banks like JPMorgan have long deployed AI for fraud monitoring and are exploring more autonomous/agentic workflows; broader industry analyses and vendor case studies show banks adopting agentic patterns for alert triage.

- DBS uses agentic AI to monitor transactions in real time and detect unusual customer behaviour. When a risk pattern appears, the agent triggers behavioural “nudges” to warn customers and escalates high-risk cases to human fraud teams for final review.

2. Personalized financial advisory

For a long time, truly personalized financial planning was accessible only to high-net-worth individuals. AI agents are changing that. They act like always-available financial co-pilots, giving everyday users the kind of tailored guidance that once required a dedicated advisor.

These agents learn from a user’s spending patterns, financial goals, and risk tolerance, and not just market data. That lets them move from passive alerts to proactive, context-aware guidance.

Proactive goal alignment: The agent monitors cash flow and assesses whether the user is drifting from key goals. If it spots something like overspending, it suggests a concrete action, not just a warning. “You’ve gone 20% over your dining budget. To stay on track, consider moving $150 from your contingency fund to savings on Friday. Approve?”

Contextual investment nudges: By analyzing the user’s portfolio alongside real-time economic signals, the agent can recommend small rebalances or adjustments while remaining within the user’s defined Investment Policy Statement (IPS).

Real-world examples:

- Betterment uses AI to craft personalized portfolios for over 1,000,000+ clients, and its automated rebalancing helps deliver some of the strongest returns among robo-advisors.

- Wells Fargo uses AI chatbots like Fargo to deliver conversational financial guidance that’s directly integrated with their planning tools.

These examples show how AI agents turn defense into offense, saving billions in potential losses.

3. Credit underwriting & instant loan origination

AI agents streamline underwriting by automating the full workflow from collecting documents, extracting features, running risk models, and checking compliance, to generating an explainable decision package. This enables near-instant lending decisions while keeping every step auditable.

Traditional underwriting is rigid and rule-based. Agentic systems make it adaptive, transparent, and scalable, especially when multiple micro-decisions are involved (income check → bank flow validation → scoring → pricing → review routing).

Agent capabilities

- Collect and enrich data from bank statements, credit bureaus, and behavioral signals.

- Run multi-model pipelines: scorecards, ML models, LLM reasoning.

- Explain each decision with a clear, traceable audit trail.

- Self-improve by analyzing past approvals and rejections.

Real-world examples:

- Specialized vendors like Zest AI and several lenders partner on AI underwriting and instant decisioning; many banks and fintechs integrate IDP + ML underwriting for faster origination.

- Bank of America’s AI assistant, Erica, scans customer cash flows to deliver instant prequalification checks, enabling decisions in under a minute.

4. Autonomous trading & portfolio optimization

In trading, milliseconds matter. AI agents can bridge the gap where human oversight falls short by scanning markets in real time, using reinforcement learning and news sentiment to inform trading and hedging decisions.

These agents function as market-aware, goal-driven financial advisors that work 24/7. By analyzing historical data and macro events, they can dynamically rebalance portfolios—shifting to defensive assets during volatility—to maximize returns while protecting capital.

Core agent capabilities:

- Live monitoring: continuously scans market feeds, news, and macro economic shifts.

- Dynamic rebalancing: adjusts holdings based on strict user constraints (risk tolerance, diversification).

- Contextual memory: retains user preferences and long-term goals to guide every decision.

- Hybrid execution: can trigger trades automatically within strict limits or generate prepared insights for wealth managers.

Example: When a specific sector becomes overexposed due to price spikes, the agent detects the risk and immediately rebalances the portfolio to restore its intended asset allocation.

Real-world examples:

- JPMorgan’s LOXM agent executes trades with minimal market impact, while hedge funds like Renaissance Technologies employ RL-based agents for low-risk portfolio tweaks.

- Numerai runs a “crowd-sourced, AI-powered hedge fund”: data scientists build ML models on encrypted financial data, stake NMR tokens based on their confidence, and the top models are merged into a “meta-model” that actually trades.

It’s not sci-fi; it’s the new normal, turning volatile markets into optimized opportunities – but it’s typically adopted later, after controls and surveillance are mature.

5. Compliance and regulatory filing automation

Compliance is often the most resource-heavy function in finance. A constant race against shifting rules, where a single missed update can mean hefty fines. AI agents change this dynamic entirely. Think of them as an always-on regulatory radar that doesn’t just beep when there’s trouble, but actually prepares the solution for you.

Instead of teams manually hunting through circulars or Basel norms, these agents continuously monitor regulator feeds. But they go further than simple alerts: they map these new obligations directly to your internal policies, identifying exactly what needs to change.

Agentic capabilities

- Stay ahead of rule changes: scan global regulations and map their impact on internal policies.

- Handle the paperwork: drafts complex regulatory reports by gathering and formatting data.

- Spot suspicious activity 24/7: flags unusual behavior that could signal money laundering or other risks.

- Create perfect audit trails: logs every action with clear evidence, references, and approvals.

Here’s how it plays out: A new anti-money laundering rule is announced overnight. By 9 AM, the compliance team logs in to find a full breakdown from their AI agent: which internal policies are now outdated, which customers are affected, and a draft policy update awaiting their review. It turns a potential crisis into a manageable morning task.

Real-world examples:

- RegTech vendors and compliance platforms (e.g., Compliance.ai and similar services) are already used by banks to monitor rules and automate parts of regulatory reporting; consultancy pieces outline agentic use cases for compliance automation.

- AUSTRAC (Australia’s financial intelligence agency) has leveraged AI tools to enhance its ability to detect and prevent suspicious activities, a clear indication that government regulators and financial institutions are integrating AI to improve the accuracy of AML and fraud reporting. The overall industry move is toward the “Agentic era of compliance.”

It’s compliance as a superpower: always on, error-proof, and audit-ready.

6. Document intelligence & financial data extraction

In banking, data is king. But what happens when your royal assets are trapped in a chaotic kingdom of PDFs, scans, and even handwritten notes? From bank statements to invoices and contracts, this “dark data” is a goldmine of insights, if only you could access it.

Enter AI agents, your specialized team for taming this paper tiger. These aren’t your average bots. By combining OCR with advanced AI, they read and interpret complex financial documents in real time.

Here’s how agents revolutionize the game:

- Intelligent extraction: parse a bank statement, pull out line items, categorize spending, and calculate key financial ratios for underwriting.

- Automated consistency checks: cross-reference a salary slip with a bank statement, instantly flagging inconsistencies.

- Seamless integration: convert extracted data into a structured format ready for credit or risk systems.

- Smart escalation: if confidence is low, flag the document for human review to ensure accuracy and reliability.

By deploying AI agents, financial institutions are finally unlocking the value hidden in their documents. They are slashing manual processing time, reducing errors, and empowering their teams with clean, actionable data for faster, smarter decisions.

Real-world examples:

- DataSnipper automates data extraction in Excel for audit workflows and is widely used by big firms to process large volumes of invoices and confirmations.

- Ocrolus’s intelligent document processing uses AI to automatically capture, classify, and extract data from financial documents like bank statements. This drastically reduces manual review, minimizes errors, and accelerates decision-making in areas like lending.

These use cases highlight AI agents as the connective tissue of modern finance—scalable, intelligent, and indispensable. From fraud sentinels to doc whisperers, they’re not replacing humans but amplifying us, driving a sector that’s more resilient and client-centric.